Client Alerts

Check-Up and Diagnosis: The Ongoing Scrutiny of Private Equity Healthcare Investments

May 06, 2025

By Emily Deagen,Bill Schwab,Josh Ratner,Jane H. Yoon,Dhara Satija

and Chloe Hillson

In 2024 alone, over 676 private equity firms and related investors acquired healthcare companies or related assets. The growing influence of private equity in the healthcare industry has not gone unnoticed on either of the federal or state levels. The trend toward increased scrutiny of private equity investments in healthcare, which started gaining traction among the states in recent years (for example, both New York and California in 2023), is increasingly apparent in legislation proposed in the last few months. Such regulatory action may be particularly appealing to states where private equity has been publicly associated with a large and noteworthy healthcare system event, such as the financial collapse of Massachusetts’ Steward Health Care in May 2024, or the closure of Pennsylvania’s Crozer Health hospital network in March 2025. Based on current state-level trends, other states may join those listed below in regulating or significantly curtailing private equity investment into the healthcare sector.

Below, we provide an overview of the current state-of-play in federal and state regulation, and offer practical suggestions for private equity investors and healthcare providers navigating deals in the current regulatory environment.

Private Equity Investments in Healthcare Remain a High Profile Federal Issue

While federal-level regulation of private equity investments into healthcare was a stated priority under the Biden administration, the current regulatory environment remains uncertain. Notably, on March 27, 2025, the Department of Justice launched the Anticompetitive Regulations Task Force for the purpose of identifying and eliminating federal and state laws that may hinder free market enterprise (which may include state-level healthcare regulations).

Even though the direction of antitrust and Department of Justice action is not clear, given the introduction of the Anticompetitive Regulations Task Force, scrutinization of private equity investments into healthcare is at least on the radar for federal enforcement. The Congressional Research Service noted that, as of August 2024, several members of Congress have “indicated interest” in such investments. In the past few months, prominent figures across the federal government have made public statements against private equity. During a February 25, 2025, hearing on the nomination of Stephen Feinberg, the co-founder of Cerberus Capital Management, for deputy secretary of defense, Sen. Elizabeth Warren (D-MA) questioned the former CEO on the private equity industry’s practice of “hollow[ing] out [our] businesses” in relation to the Steward Health Care collapse. Across the aisle, although not an attack on healthcare investments specifically, President Donald Trump has publicly vowed to eliminate the carried interest “loophole,” while the current Secretary of Health and Human Services Robert F. Kennedy Jr., during his run for president, called private equity investments “theft by billionaires” that “has to stop.” Although words from politicians may not equate to prompt regulatory action, both political parties have directed heated rhetoric at private equity firms and seem emboldened to continue to do so.

State-Level Regulation on the Rise

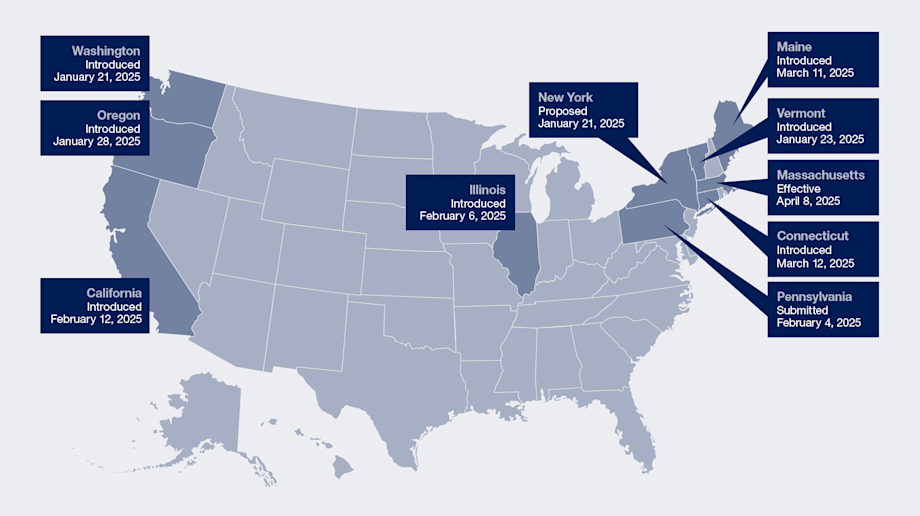

In addition to federal regulatory action, as of the time of publication of this article, in calendar year 2025 alone, at least 10 states are considering or have already passed bills to limit, ban or otherwise regulate private equity investment in the healthcare sector. Many of these states have higher-than-average healthcare spending and would otherwise be attractive for private equity investment.

Most proposals for state legislative reform seek to deter private equity investment by limiting the roles of private equity firms and management services organizations (MSOs) in healthcare. Some states, such as Maine, Connecticut and Washington, have proposed laws that would fully prohibit private equity groups or non-licensed healthcare providers from either owning, acquiring or increasing their existing ownership interests in healthcare entities, while others leverage lengthy notice and review timelines (including up to 180 days in Vermont and New York) that may dissuade transactions.

Key legislative updates relevant to private equity firms in the healthcare industry are summarized by state below (current as of May 1, 2025):

|

State |

Name/Number, Title, Date and Status |

Summary of Key Points |

|

Massachusetts |

Chapter 343 of the Acts of 2024 (H.B. 5159 – An Act Enhancing the Market Review Process) Signed by Gov. Maura Healey on January 8, 2025; effective April 8, 2025. |

H.B. 5159 increases transaction oversight by broadening the definition of “material change” to capture transactions involving “significant equity investors,” non-profit to for-profit conversions and significant acquisitions, sales or transfers of assets. Further, H.B. 5159 allows the Massachusetts Health and Policy Commission to perform a cost and market impact review if it identifies that a transaction may reduce competition or increase spending and, in its discretion, may refer results to the state attorney general for action. The law additionally increases reporting requirements, including an annual statement detailing ownership, finances, corporate affiliates and out-of-state operations. Expands the scope of the Massachusetts False Claims Act to pass through liability to upstream owners of healthcare providers for violations of the Act. |

|

Oregon |

(Relating to the Practice of Health Care; Declaring an Emergency) Introduced in Senate on January 28, 2025; passed by Senate and referred to House on April 8, 2025. |

S.B. 951 aims to prohibits MSOs and their affiliates—such as independent contractors, shareholders, directors, officers and employees—from owning, controlling or managing a medical entity with which they contract. S.B. 951 would further ban noncompetition, nondisclosure and nondisparagement covenants between medical professionals and corporate entities, and declares that violations of this legislation will be treated as unlawful trade practices under state law. |

|

Connecticut |

(An Act Prohibiting Private Equity Ownership and Control of Certain Health Care Institutions and the Controlling of or Interference with the Professional Judgment and Clinical Decisions of Certain Health Care Providers and Requiring an Evaluation of the Appointment of a Receiver to Manager Hospitals in Financial Distress) Introduced in Senate on March 12, 2025; calendared with Senate on April 9, 2025; introduced in House on March 14, 2025.

|

S.B. 1507 aims to codify existing corporate practice of medicine-related restrictions to prevent influence of private equity in the independent professional judgment of licensed medical providers. S.B. 1507 would prohibit private equity groups from acquiring or increasing any direct or indirect ownership interest in, or financial or operational control over, a healthcare provider. |

|

|

(An Act Expanding Liability under the False Claims Act for Entities with an Ownership Interest and Prohibiting the Licensing of Hospitals with Certain Lease Back Arrangements) Introduced in House on March 14, 2025. |

H.B. 7224 proposes expansion of the State False Claims Act to impose liability on a person with ownership or investment interest in an entity that violates the act if such person knows of and fails to report a violation within 60 days after knowing of such violation. |

|

Maine |

(An Act to Impose a Moratorium on the Ownership or Operation of Hospitals in the State by Private Equity Companies or Real Estate Investment Trusts) Introduced in Senate on March 11, 2025. |

The proposed law would ban any private equity company from acquiring or increasing a direct or indirect ownership interest, operational control or financial control in any hospital in the State of Maine through June 15, 2029. |

|

California[1] |

(California Health Care Quality and Affordability Act) Introduced in Assembly on February 21, 2025. |

The California Health Care Quality and Affordability Act (A.B. 1415) seeks to require private equity firms and MSOs to notify the Office of Health Care Affordability (OHCA) of certain healthcare transactions under the current OHCA law. |

|

|

(Health Facilities) Introduced in Senate on February 12, 2025. |

S.B. 351 seeks to codify existing guidance on restrictions on the corporate practice of medicine and gives the state attorney general a new enforcement mechanism by explicitly prohibiting private equity groups from taking any action that could influence or exert control over the professional judgment of physicians in making healthcare decisions. |

|

Illinois |

(Amends the Illinois Antitrust Act. Requires the attorney general to consent to covered transactions of health care facilities before a covered transaction may take effect.) Introduced in Senate on February 6, 2025. |

S.B. 1998 seeks to amend the Illinois Antitrust Act to require prior written consent from the state attorney general for transactions involving investment into healthcare facilities or provider organizations where any of the transaction financing is provided by a private equity group or hedge fund. Currently, the Illinois Antitrust Act only requires notification of the state attorney general. |

|

Pennsylvania |

Gov. Josh Shapiro’s Executive Budget for 2025–2026 Submitted to General Assembly on February 4, 2025; as of time of publication, Executive Budget is in Appropriation Committees Hearings. |

Gov. Shapiro’s proposed Executive Budget makes the request for state legislators to allow the state attorney general to review (and block) hospital and nursing home sales, mergers and acquisitions. In the wake of the March 2025 closure of Pennsylvania’s Crozer Health hospital system, other state representatives have spoken out to decry private equity’s perceived role in the closure, and bills limiting investment are expected to be introduced in the General Assembly in the upcoming months. |

|

Vermont |

(An act relating to health care entity transaction oversight and clinical decision making) Introduced in House on January 23, 2025. |

H.B 71 seeks to impose new restrictions on healthcare ownership and transactions by prohibiting (i) shareholders, directors and officers of healthcare practices from owning or holding certain positions in a contracted MSO and (ii) licensed providers from transferring ownership of a medical entity to individuals or entities who are not licensed providers. Further, H.B. 71 would require healthcare entities to give notice to the Green Mountain Care Board, a regulatory board appointed by the governor, at least 180 days prior to the date of certain transactions, upon which the board and state attorney general will have 30 days (180 days if more comprehensive review initiated) to review and approve, approve with conditions or reject the transaction. |

|

New York |

Gov. Kathy Hochul’s Executive Budget for FY 2026 Proposed to Senate and Assembly on January 21, 2025. |

Gov. Hochul’s proposed Executive Budget includes a new procedure that would require parties to submit notice of certain transactions 60 days in advance of closing such transactions and grants the Department of Health the ability to conduct a preliminary review and, in its discretion, a full cost and market impact review, which may delay transactions up to 180 days. |

|

Washington |

(An Act Relating to the Corporate Practice of Medicine) Introduced in the Senate on January 21, 2025. |

S.B. 5387 seeks to allow only licensed individuals or entities to own or control healthcare practices unless state law explicitly allows otherwise. Washington-licensed healthcare providers would be required to maintain control of such practices by holding a majority of shares, serving as a majority of directors and occupying key leadership roles. Further, S.B. 5387 seeks to bar other individuals or entities involved in healthcare practices—such as shareholders, directors and officers—from owning equity in or working for a contracted MSO or receiving significant financial compensation in exchange for ownership or management of the medical practice. Such individuals or entities also may not transfer control of shares or dividends in the practice. |

Navigating the Changing Regulatory Landscape

With many prospective state (and potentially federal) changes on the horizon, it is important for private equity investors to be thoughtful when considering an investment in a healthcare asset. Each transaction will have its own particular challenges and uncertainties, but the below considerations can be a helpful starting point to analyze whether and how to make investments into the healthcare sector.

- Consider transaction characteristics to realistically assess risk.

- Geography: Certain states are seen as “investor-friendly” jurisdictions, but state regulations can change quickly and with little advance warning. Investments into states with attorneys general or other regulators that have made public statements against private equity investment in healthcare, or private equity more generally, may be at an obviously higher risk of scrutiny by state authorities. Relatedly, one of the major areas of concern vocalized by state regulators has been access to medical care in rural or underserviced communities. Government officials may focus on transactions that have the potential to negatively impact local communities and vulnerable patient populations.

- Type of Healthcare Asset: Generally, investments into healthcare assets such as hospitals or physician practices have been scrutinized more than medical technology or health insurance payer transactions. State regulations mainly target investments into entities that provide healthcare and have not (yet) expanded into healthcare services and technology sectors (although, as of the time of publication, both New Hampshire and Oregon can block health insurance carrier transactions). As a result, acquisitions of or investments in nonprofit hospitals are the most heavily regulated and often the process with the most hurdles to clear.

- Investment Structure and Control: In states with existing regulatory regimes focused on the vertical, the vast majority of private investments in healthcare are subject to at least some notice or review. While some state statutes have materiality thresholds that let small-dollar investments avoid regulatory review, Colorado, Connecticut, New Mexico, Rhode Island and Vermont have no such materiality thresholds for review, as of the time of publication. However, even non-control or non-“material” investments (including hospital joint ventures) in certain states may have a lower level of scrutiny depending on the precise language of the law. Many current and proposed statutes hinge on control elements (e.g., voting control, board control), and thus state-dependent structuring of investments to limit control elements can be advantageous if working on a tight timeline or attempting to manage reporting in a regulated state.

- Budget time for (and be practical about) enhanced regulatory review and federal antitrust review.

- State Regulatory: The general timeline for state review ranges from 30 to 90 days depending on the jurisdiction. Unfortunately for deal professionals, the rules for when and how a state agency can request additional information and refer a transaction for attorney general review can be amorphous, with uncertain timing. Consider whether the typical termination provisions (e.g., regulatory denial, outside date) in the main transaction agreement will allow for a delay. From a practical standpoint, it is worth discussing at the term sheet stage and making a plan for a realistic timeline to closing.

- Federal Antitrust: In transactions that involve practices or hospitals, time for Hart-Scott-Rodino second requests may need to be budgeted into the closing process. Additionally, early indications suggest that acquisitions of competitive businesses will be scrutinized to a similarly aggressive degree as under the prior administration.

- Consider whether to engage in enhanced regulatory and compliance due diligence.

In addition to preparing for enhanced regulatory review, transacting parties should consider whether to do a deeper dive into specific regulatory and compliance topics that may be scrutinized by regulators. As regulator interest heightens, compliance with healthcare laws has moved to the center stage of due diligence efforts. It is important to budget additional time for regulatory and compliance due diligence review and set realistic expectations in terms of timeline, especially in the current environment where regulation priorities can change quickly and without warning. The scope, approach and timing of the due diligence review will vary based on the type and size of healthcare asset, and investors and healthcare companies should consult with their legal team and other diligence providers to develop a comprehensive plan for conducting due diligence. A thorough due diligence process, including review of compliance with applicable federal and state regulations and analysis of the company’s historical compliance programs, will inform risk management needs, post-transaction priorities and overall investment value.

- Prepare strategically for reporting to state agencies.

In states with an established regulatory review of healthcare private equity transactions, preparing to invest into a healthcare practice or hospital requires forethought in what materials to prepare and present to regulators. Consider whether any materials or information would be subject to public disclosure, and whether any should be held confidential as proprietary information by state regulators. This designation usually has to be made prior to submission of relevant documentation, so parties should be mindful and consult with counsel when producing information for regulators.

Finally, even though the most onerous reporting obligation will come at the time of transaction approval, many states with regulatory regimes have ongoing reporting requirements (for example, the new Massachusetts law requires annual reporting by healthcare providers, investor groups and MSOs). This ongoing reporting relationship will be different from other one-and-done regulatory approval processes with which investors are familiar, and such investors may need to be prepared for the potential for repeated contacts with the same regulators and their offices on an annual or even quarterly basis. These regulators may review the acquired business and the private equity owners multiple times throughout the investment hold period and upon the sale of the business, so private equity investors should view the regulation process as a long-term relationship. The importance of patience, cooperation and a collaborative attitude towards state regulatory offices cannot be overstated.

Conclusion

Whether it be notice and review requirements, investment limitations or outright bans on private equity acquisitions, recent state trends toward (and federal level discussions regarding) regulation of private equity investment in healthcare necessitates strategic planning before, during and after a transaction. No matter how the regulatory environment for private equity investments in healthcare evolves at the federal and state levels, the attorneys and healthcare consulting team at Paul Hastings remain committed to providing expert guidance and comprehensive advice tailored to these developments.

[1] Both California bills reintroduce provisions similar to those in Assembly Bill 3129, which was vetoed by Governor Gavin Newsom in Fall 2024. These pending bills may be similarly vetoed by Newsom, but may be overridden by a two-thirds vote in each of the Senate and the Assembly (although an override has not occurred since 1979).

Contributors

Managing Director, Life Sciences & Healthcare Consulting Group

Practice Areas

For More Information

Managing Director, Life Sciences & Healthcare Consulting Group